What is the Impact of a Policy Loan under Direct Recognition?

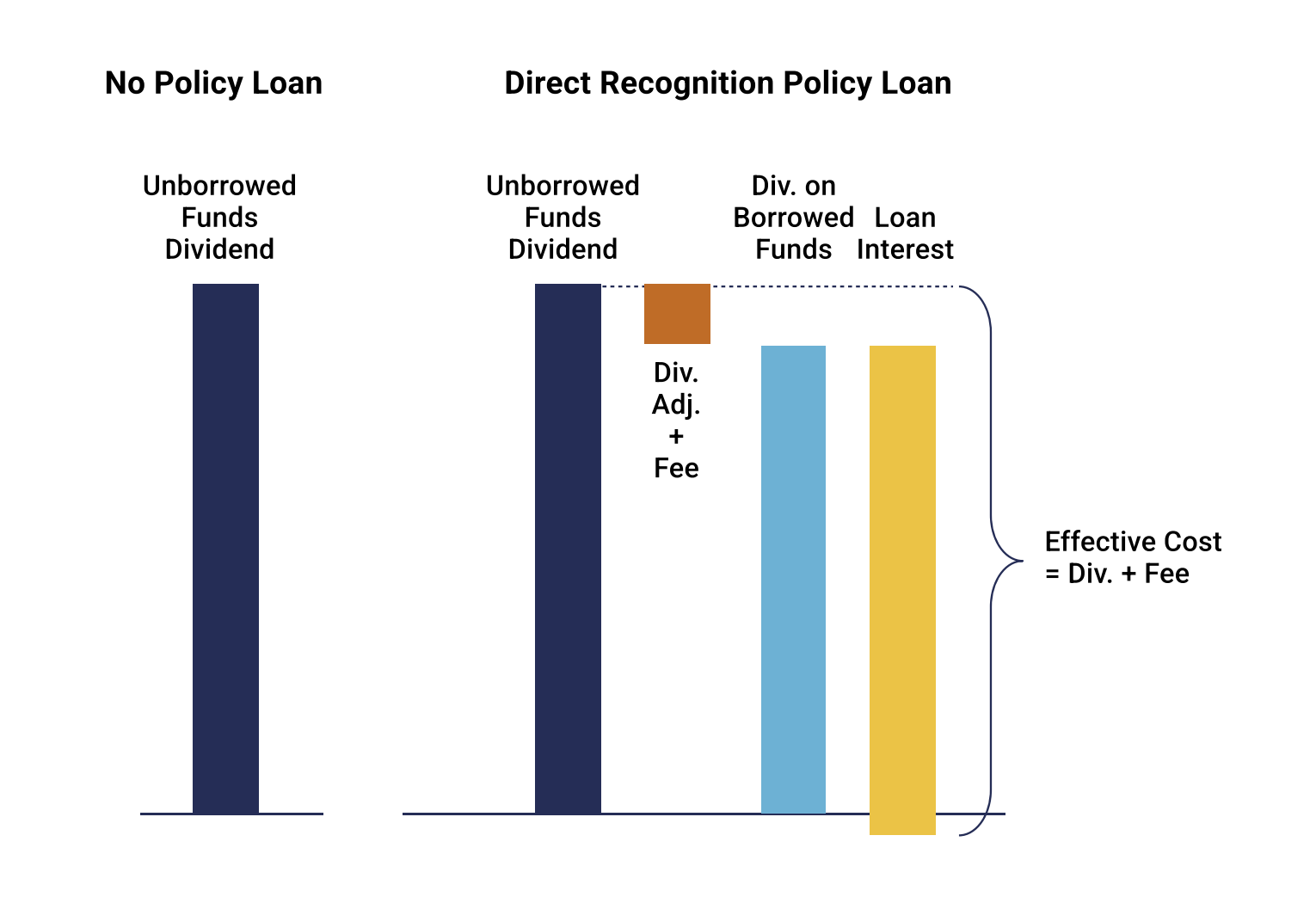

The answer is not as straightforward as you may think. Direct recognition means the insurance carrier has separate dividend rates for borrowed and unborrowed cash value – under Non-Direct Recognition all policies earn an equal dividend rate, regardless if there is a loan outstanding.

The specific details vary, but most carriers apply an adjustment to the dividend earned on borrowed funds with the goal of aligning the interest earned from the policyowner with the investment return the carrier would have made had the funds not been borrowed, plus a small spread to cover administrative costs of borrowing.

Direct Recognition carriers adjust dividends to align the interest earned with the investment return they would have made. In other words, the cost of a policy loan is the foregone dividend plus a small fee, regardless of the rate listed on the policy.

Since the dividend is adjusted to align net borrowing cost with returns, the loan interest rate specified in the contract is typically immaterial to the actual impact of a policy loan.

For example, in 2025 Northwestern offers both an 8.00% fixed rate and a variable Market Loan Rate, currently 5.73%. However, due to the different dividend adjustments the total cost of borrowing is identical in either case: 5.75%, the 5.50% dividend plus a 0.25% charge (charge varies 0.25% to 0.65% by policy age).

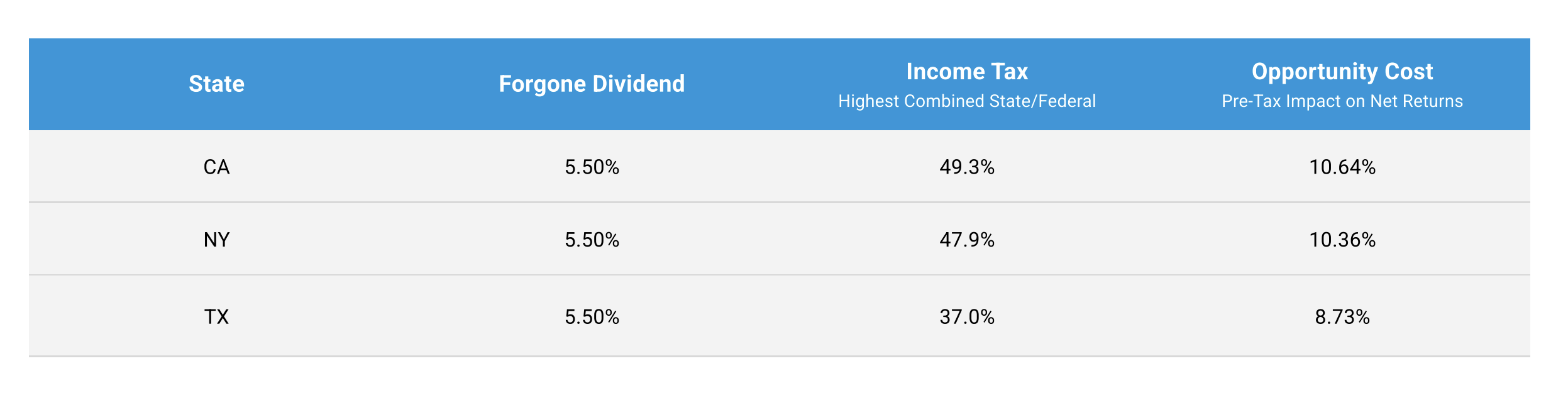

What is the True Cost of Foregoing the Dividend?

One key benefit of Whole Life Insurance is that it can provide the same after-tax return of an investment with a higher pre-tax return, but without the higher investment risk and volatility associated with other asset classes.

That attractive after-tax return is achieved through the dividend, which is given up when funds are accessed via policy loan. For high income earners anywhere, but especially in states with high state income taxes, the opportunity cost can be quite meaningful:

For example, a client in Los Angeles whose dividend is earning the pre-tax equivalent of 10.64% should not be willing to trade away that return for anything less than 10.64%. When it comes to borrowing, if the client can access funds outside the policy for less than 10.64%, then keeping the dividend can be a better option.

The pre-tax impact of a policy loan can be 8.73% to 10.64% for high earning clients due to the loss of the dividend. Third party lenders, such as Inclined, allow policyowners to continue to earn the attractive tax advantaged return of the dividend.

Additionally, interest paid on policy loans is clearly not deductible, however interest paid on loans made by a third party may be deductible if used for certain purposes1.

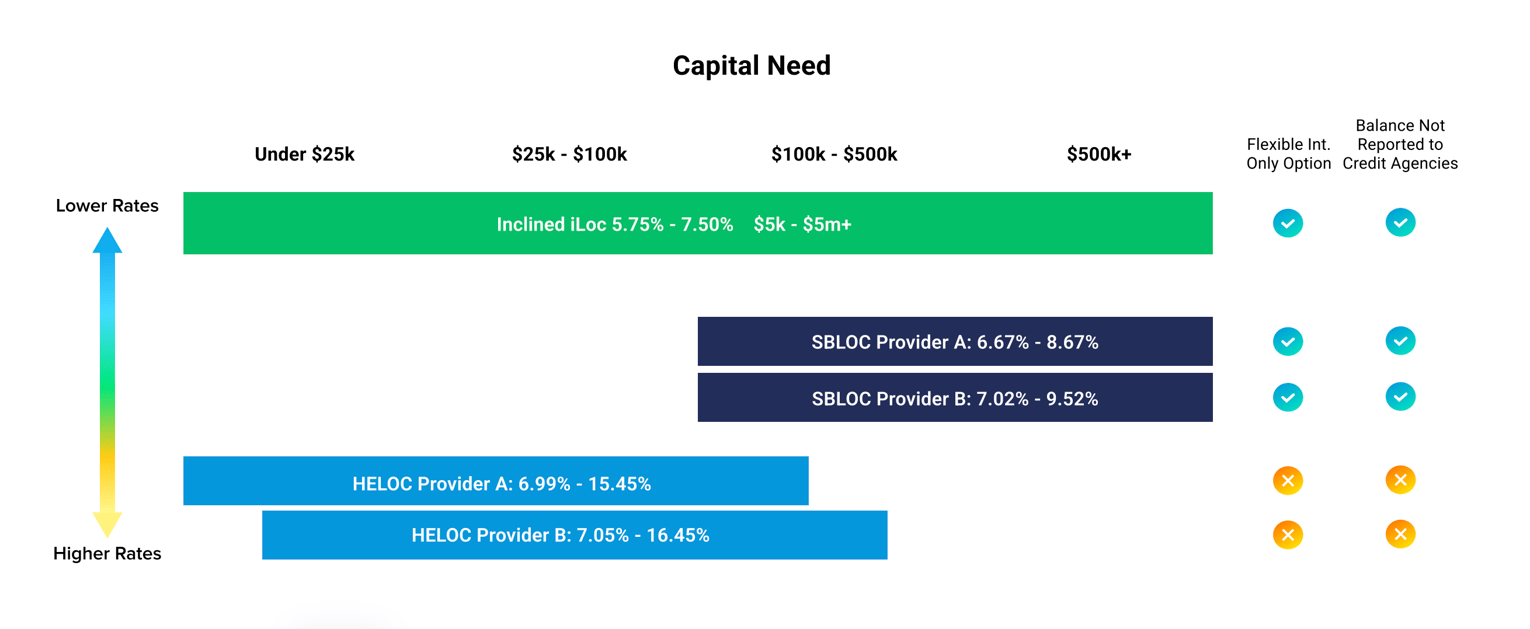

Third-Party Cash Value Loans vs. Other Borrowing Options

To protect the post-tax returns earned inside the dividend from the negative impact of a policy loan, clients likely want to consider borrowing outside of the policy. When considering where to borrow, policyowners have a number of options.

As of December 2024, few options offer better rates and flexibility, for both small and large line sizes, than borrowing against cash value via a third party.

SBLOC provider A is Charles Schwab PAL product as of Jan.22,2025 at SOFR + 2.40% to 4.40%, minimum of $100K. SBLOC provider B is Raymond James SBLOC product as of Jan. 22, 2025 at SOFR + 2.75% to 4.60%, minimum of $100K. HELOC Provider A is Aven’s stated APR range as of Dec. 4, 2024 with $5k-250K line sizes. HELOC Provider A is Figure’s stated APR range as of Dec.4,2024 with $15k-400K line sizes.

The Inclined Line of Credit (iLOC) is a revolving line of credit designed to give whole life policyowners the ultimate freedom and flexibility to access the cash value in their policies. We’ve innovated to offer features and benefits that include:

-

Apply online in 15 minutes or less2

-

Access up to 95% of cash value3

-

Next-day draws4

-

Minimum $5,000 credit limit5

-

Evergreen lines, no manual renewals

-

Automatic evaluations for credit limit increases6

-

Not reported to credit bureaus

-

Competitive rates

-

No fees, ever

Download a PDF version of this case study to share it easily.

Ready to get started with Inclined? Take the next steps to join our Advisor Portal or apply for an Inclined Line of Credit (iLOC) today.

1. Inclined does not offer tax advice. Please consult a tax advisor to determine deductibility in each case.

2. Typical application times are 15 minutes. Application review and approval times are typically 1 business day, and funds can be available as quickly as 10 business days from completing an application. However, time estimates are contingent upon insurance carrier response times and may be longer.

3. Credit limits can be up to 95% of the cash surrender value, not to exceed the maximum loan amount from your carrier, inclusive of existing balances. Inclined will also reevaluate your credit limit for you two times per year.

4. Once an Inclined Line of Credit is opened, policyowners can use our online portal to make draws that process overnight. Funds arrive at the receiving bank the next business day, fund availability subject to receiving bank’s policies. In some cases, it may take 2 business days.

5. Final underwritten line must be at least $25,000 in Washington D.C., $10,000 in New Mexico and Arizona, and $5,000 everywhere else.

6. When an iLOC account is active and in good standing, Inclined evaluates the credit limit twice per policy, per year and generally increases it with the value of the policy. However, credit limit increases are discretionary and are not guaranteed.

.png?width=674&height=450&name=Jillian%20(1).png)