Not All Premium Frequencies Are Created Equal

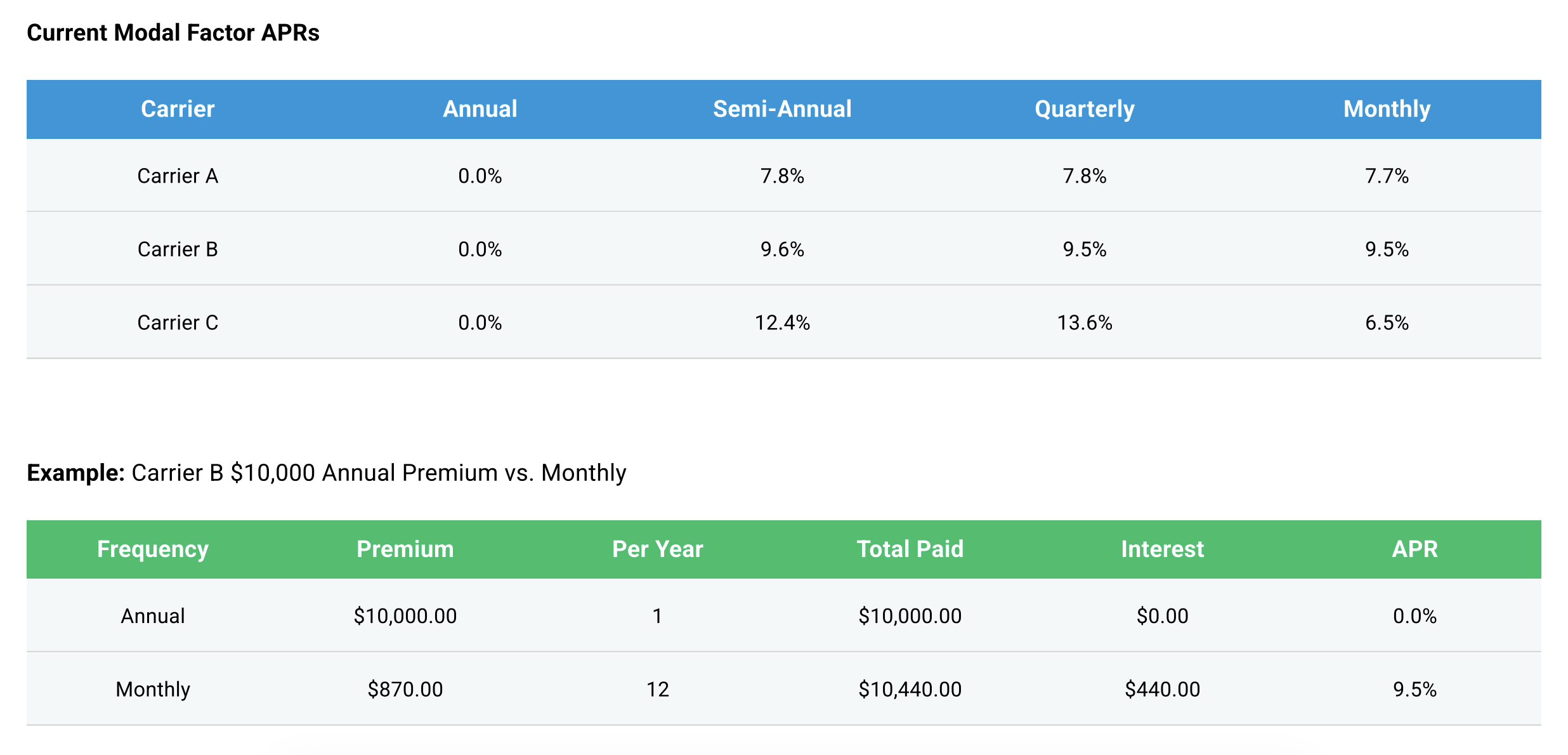

The way a whole life policyowner pays their premium matters more than you might think – when a policyowner elects to pay more often than once per year, they are effectively taking a one year loan from the policy’s insurance carrier, which they pay back in 2, 4, or 12 payments. These “loans” have interest, typically called Modal Factors, and can amount to APRs over 13%, all for the convenience of paying in smaller installments for the exact same coverage and cash value growth.

If a policyowner pays the premium as a lump sum, there are no interest charges. If they prefer to pay monthly, quarterly, or semi-annually, using an Inclined Line of Credit can mitigate some of the cost, while opening possibilities for additional financial growth.

What are Modal Factors?

Modal factors are effectively the interest a policyowner pays when they elect any payment mode other than annual. Policies that are paid monthly are extremely common.

Carriers A, B, and C are top 20 US life insurance carriers based in Milwaukee (WI), Springfield (MA), and New York (NY) respectively.

How Does Inclined Help?

Inclined offers a revolving, evergreen line of credit — the iLOC — that uses the cash value of whole life policies as collateral. The iLOC features an easy application, overnight online draws1 & payments, advanced autopay, competitive rates, and never charges any fees to policyowners.

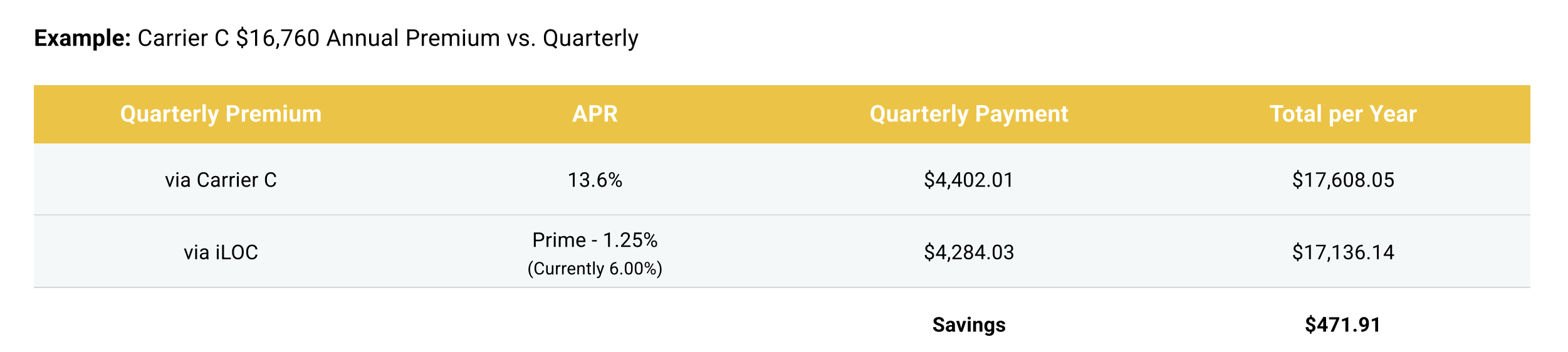

Inclined’s rates, as low as Prime minus 1.25%, are typically lower than the interest charged on monthly, quarterly, or semi-annual premium modes. A policyowner can use their iLOC to pay the premium annually, then make regular payments to their iLOC instead of to the carrier. They will pay on the same frequency they do today, and their policy will grow just the same, but payments are typically smaller and can save money.

In our example, a 35 year old purchasing a policy with $1M of initial death benefit and premiums paid until age 65 would save $471.91 per year due to Inclined’s lower interest rates:

Assumes premiums and iLOC payments are made on the first day of each quarter and statement periods are aligned to quarters.

If the policyowner took the $471.91 they saved each year by paying the quarterly premium via Inclined and invested in the S&P 500, here’s what their position looks like heading into retirement at age 65.

Assumes $471.91 invested Jan 1 each year and held, investment performance follows actual S&P 30 year annual gains 1996-2025.

How Do Policyowners Start Saving Money On Premiums With Inclined?

Most — but not every — policy configuration will save money with Inclined, so consult the tables below or ask a Financial Advisor.

There are four simple steps to start saving money on your premiums with Inclined:

-

Open an Inclined Line of Credit (iLOC) on the policy

-

Switch the policy’s premium mode to annual

-

Login and make a draw from the iLOC to pay the premium

-

Make the payments that would normally go to the carrier on the iLOC. This can be done in one of two ways:

-

Set up Autopay. By default, Autopay on iLOCs with existing balances will include all interest from premiums and prior balances. Change it to set Autopay to pay the interest plus principal (e.g. 1/12 for monthly); or

-

Login and make regular payments. To calculate your payment use the tables in the appendix, adjusted for your premium amounts

-

That’s all it takes to start saving!

More About the Inclined Line of Credit

Inclined gives whole life insurance policyowners a cost-effective, simple way to access the cash value they have built in your policies. The Inclined Line of Credit (iLOC) is easy to apply for, easy to use, and designed to give them the ultimate freedom and flexibility when accessing your cash value. Top features of the iLOC include:

-

Evergreen line - Policyowners will never need to re-apply to renew their line of credit. Once it's open, it'll stay open as long as the policyowner wants it.

-

Overnight draws2 - Link a bank account to an iLOC to draw funds quickly from the account online.

-

Automatic credit limit evaluations - As the policy’s cash value grows, Inclined will automatically evaluate the line for credit limit increases3.

-

Not Reported to Credit Bureaus4 - Inclined does not report iLOCs as outstanding debt to the credit bureaus.

-

No fees, ever - Inclined doesn't charge you fees for your line, whether you use it or not.

Download a PDF Version of this case study to view additional Policy Configurations and Savings charts in the Appendix.

Carriers A, B, and C are top 20 US life insurance carriers based in Milwaukee (WI), Springfield (MA), and New York (NY) respectively.

1. Once an Inclined Line of Credit is opened, policyowners can use our online portal to make draws that process overnight. Funds arrive at the receiving bank the next business day, fund availability subject to receiving bank’s policies. In some cases, it may take 2 business days.

2. Once an Inclined Line of Credit is opened, policyowners can use our online portal to make draws that process overnight. Funds arrive at the receiving bank the next business day, fund availability subject to receiving bank’s policies. In some cases, it may take 2 business days.

3. When an iLOC account is active and in good standing, Inclined evaluates the credit limit twice per policy, per year and generally increases it with the value of the policy. However, credit limit increases are discretionary and are not guaranteed.

4. To verify someone qualifies for an Inclined Line of Credit, we will request authorization for a soft credit pull that will not affect their credit score. If they later agree to a line of credit, we will pull a hard credit report that may impact their score. We will tell them before this happens.

.png?width=674&height=450&name=Jeremy%20(1).png)